Summary of Key Points

- Shared Equity Scheme applies to new build properties, self-builds and second hand properties only where tenants are purchasing the property they are renting following an eviction notice

- Only for First Time Buyers

- Participants can borrow the maximum amount available to them from one of the Participating Lenders (up to 4 times their income)

- Up to 30% of the property price

- It is an interest free loan from the government for 5 years

- You will have to pay back the share based on current market valuation at the time/ or when selling the property

- Max Purchase Price limits set by county (up to 500k)

- Can be used together with the Help to Buy (HTB) Scheme (reduced share to 20%)

- HTB is free money based on how much tax and DIRT tax you paid over the last 4 years, Shared Equity is a government loan, not free money

- Three participating banks so far – PTSB, AIB, BOI

- Applicants must have a Mortgage Approval with a Participating Lender

_____________________________________

The First Home Scheme is part of the Government’s Housing for All Plan 2030 , Affordable Housing Act, 2021. In 2021, 2 new affordable purchase schemes were announced. A local authority scheme (operated by your local council) and a national scheme (First Home Affordable Purchase Shared Equity Scheme) which was launched the 7th of July 2022.

To see if you are eligible for the scheme by using the eligibility calculator click here.

To apply for the First Home Scheme click here.

What does the First Home Scheme Do?

The Fist Home Scheme helps first time buyers who are priced out of the market to purchase or build a new build property. Under the scheme, the State will pay up to 30% of the cost of the new home (a maximum of 20% if Help-to-Buy is used) in return for a stake/share in the home equivalent to the level of funding provided.

If you wish, you can buy back the stake at any time, but you don’t have to. However, if you sell the property, you will need to return the share back to the State. For example, if you got 20% of the purchase price under the scheme, at sale, you return 20% of the sale price.

The following interest rates will apply to the equity share:

0-5 years: 0%

6-15 years: 1.75%

16-29 years: 2.15%

30+ years: 2.85%

Who is Eligible for the First Home Scheme?

The First Home Scheme is only open to first time buyers who have a Mortgage Approval with a Participating Lender. Participants can borrow the maximum amount available to them from one of the Participating Lenders (up to 4 times their income). A minimum deposit of 10% of the property purchase price is also required. The scheme is not open to self-builds, second hand properties or buy-to-lets. If you can get approved for enough mortgage and deposit to purchase a property, you are not eligible for the scheme.

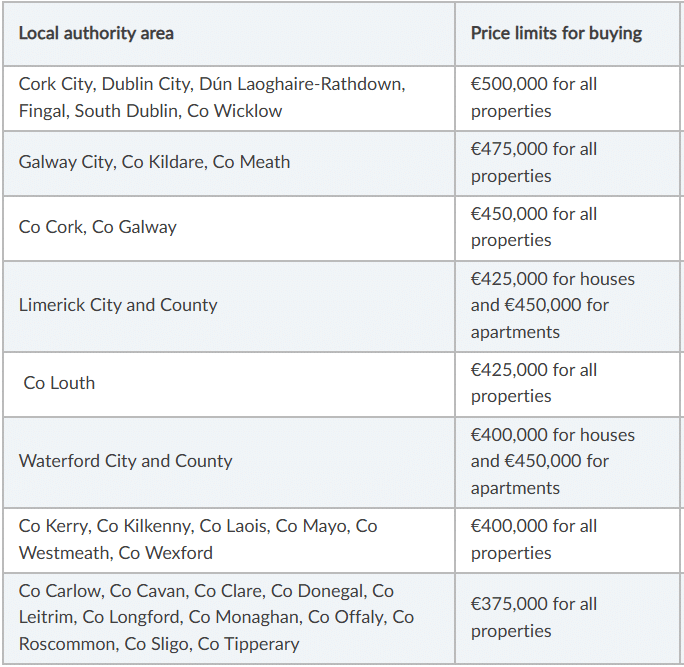

What Are the Limits for Eligible Properties under the First Home Scheme?

The properties must be new-build houses or apartments at a price of up to certain limits based on location. Prices will range from about €325,000 to €500,000.

Table 1 Price caps for the First Home Scheme 2026

More details of the First Home scheme are available on https://www.firsthomescheme.ie/

To apply for the First Home Scheme click here.